Forget the Analysts: Gold is the Unfiltered Oracle of Global Political and Economic Turmoil

Gold’s rise isn’t just a market trend—it’s a glaring signal of unfolding global upheaval.

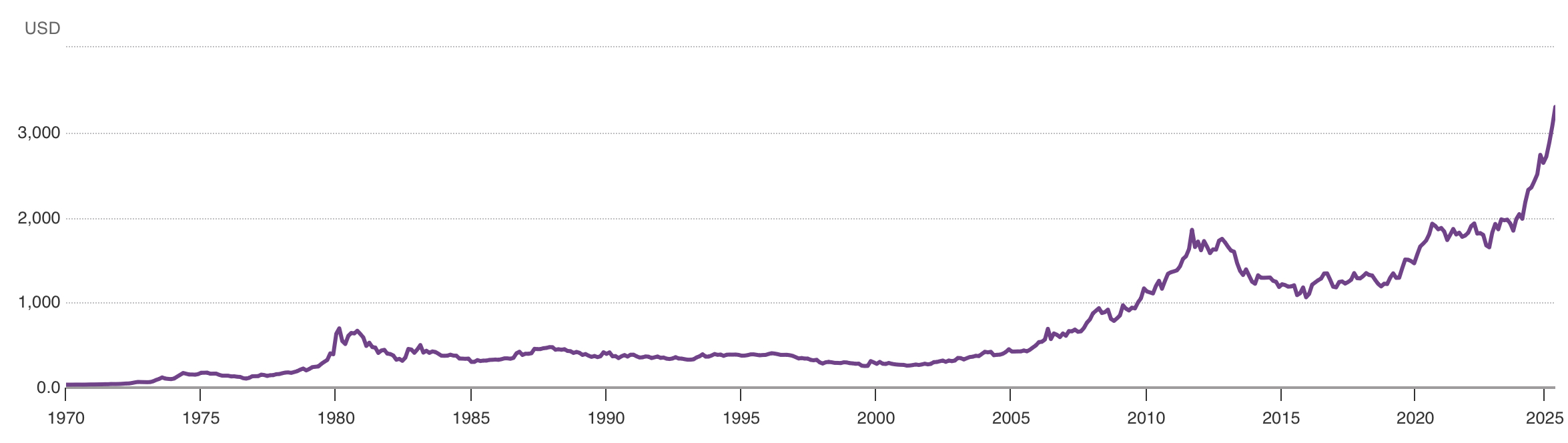

Gold’s ongoing bull run, as illustrated by the chart below, is garnering the attention of analysts and investors alike, which is not surprising given their proclivity to focus on ascending asset prices rather than on intrinsically cheap valuations.

For at least decade, the yellow metal has been signalling that radical changes were coming to the world’s post-World War 2 geopolitical and economic architecture well ahead of the foreign policy pundits, economists and investment banks.

Following the collapse of the gold price in 2011, it began a gentle upward, albeit choppy, trend since 2016.

That coincided with the election of Donald Trump as president in November 2016, the application of US tariffs on Chinese merchandise exports due to proliferating US-China hostility and the overwhelming rejection of the 11-nation trade-liberalising Trans-Pacific Partnership agreement by Democrats and Republicans alike.

Central Banks

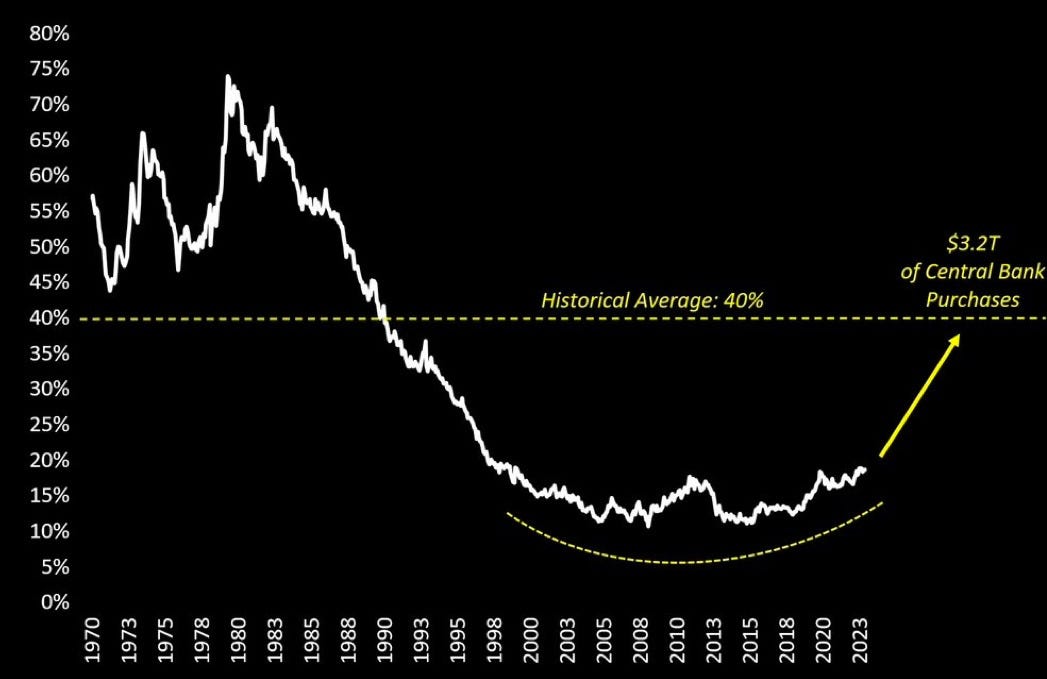

So, what drove the gold price to start its journey of uplift since 2016? Central bank buying, particularly by The People’s Bank of China at the forefront but joined by the Bank of Russia and other counterparts in Asia.

We can observe in the chart below that gold as a percentage of global international reserves held by central banks has been steadily increasing from 2016 at roughly the same time as the forward march of the gold price.

Why is that an important development? Because central banks, by nature, engage in deep and careful analysis regarding decisions on altering the composition of their reserves. They projected astutely the long term implications of the election of a populist non-establishment figure as US president.

And Trump’s assumption of the presidency, undoubtedly, did herald the US pivot away from free trade and globalisation culminating in the tariff war unleashed in his second term.

His Democratic predecessor Joe Biden pursued the same mercantilist and protectionist path. He implemented restrictions on the sale of high-end semiconductor chips to China while adopting industrial policies with a buy-America bias to boost the domestic production of chips, Electric Vehicles, solar panels and wind turbines.

Gold and US Public Debt

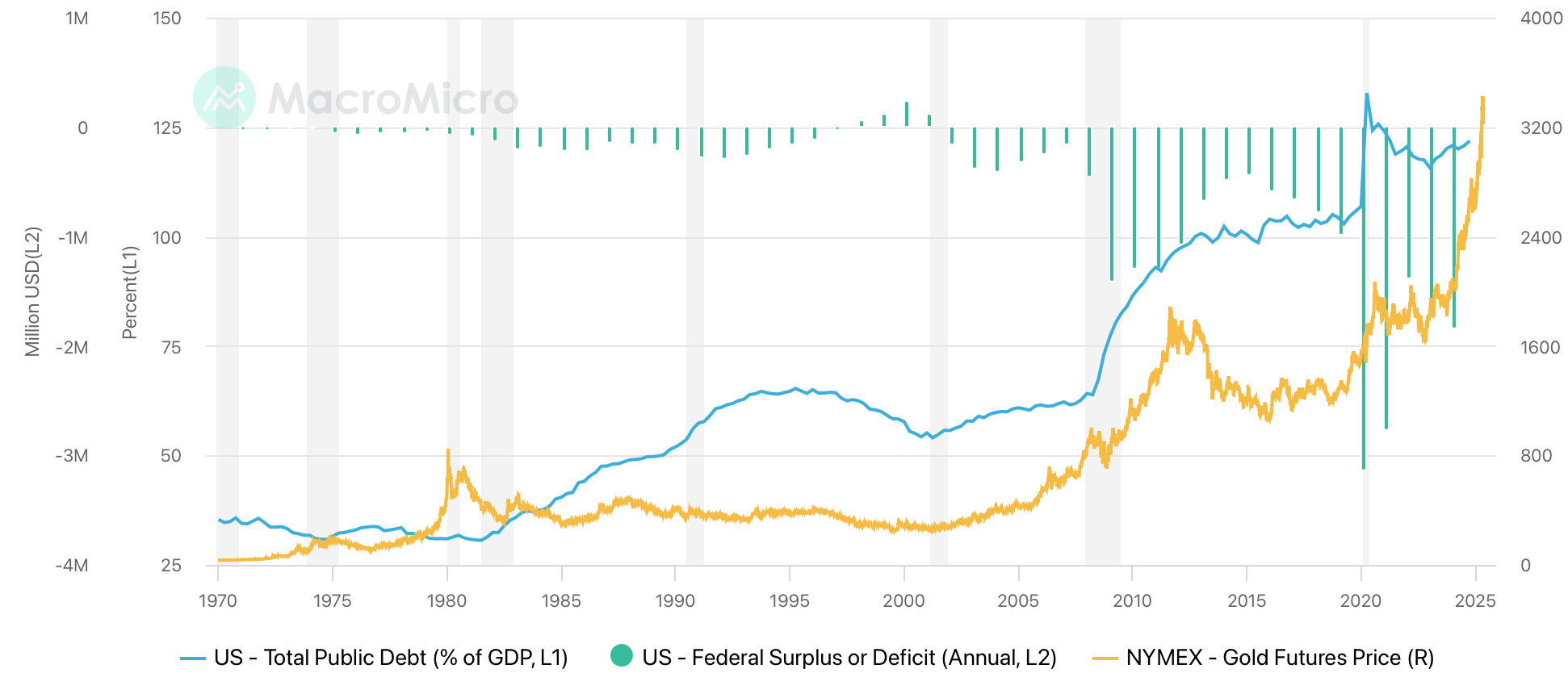

Not only did gold anticipate anti-globalisation sentiments, it also expressed concerns towards the explosion of the US federal debt at least a decade before “experts” raised the red flag on its unsustainable nature.

Juxtaposing the gold price against the US federal budget deficit and debt levels reveals that gold buyers feared, again since 2016, the incessant parabolic direction of America’s insatiable appetite for borrowing and spending.

Investors are fretting that the deteriorating US fiscal picture will compel the authorities to print it away via higher inflation, otherwise known as the “inflation tax”. In a scenario where the purchasing power of the mighty Dollar tumbles, gold’s role as a hedge and protector of wealth shines brighter than ever.

Weaponisation of the US Dollar

A third factor motivating the gold price is the incessant imposition of US economic and financial sanctions against countries, entities and individuals deemed inimical to its foreign and security interests. These actions, undoubtedly, encourage diversification into gold as a consequence of its historical reputation as a monetary metal and free of counterparty risk.

Revealingly, the tempo of sanctioning accelerated somewhat from 2016 and then decisively in 2021 onwards roughly in line with gold price movements during the last decade.

What Is Gold Telling Us Now?

Gold is informing us quite loudly and forcefully that some seismic geopolitical, financial and economic developments will be unfolding in the short-to-medium term with durable and long-lasting implications.

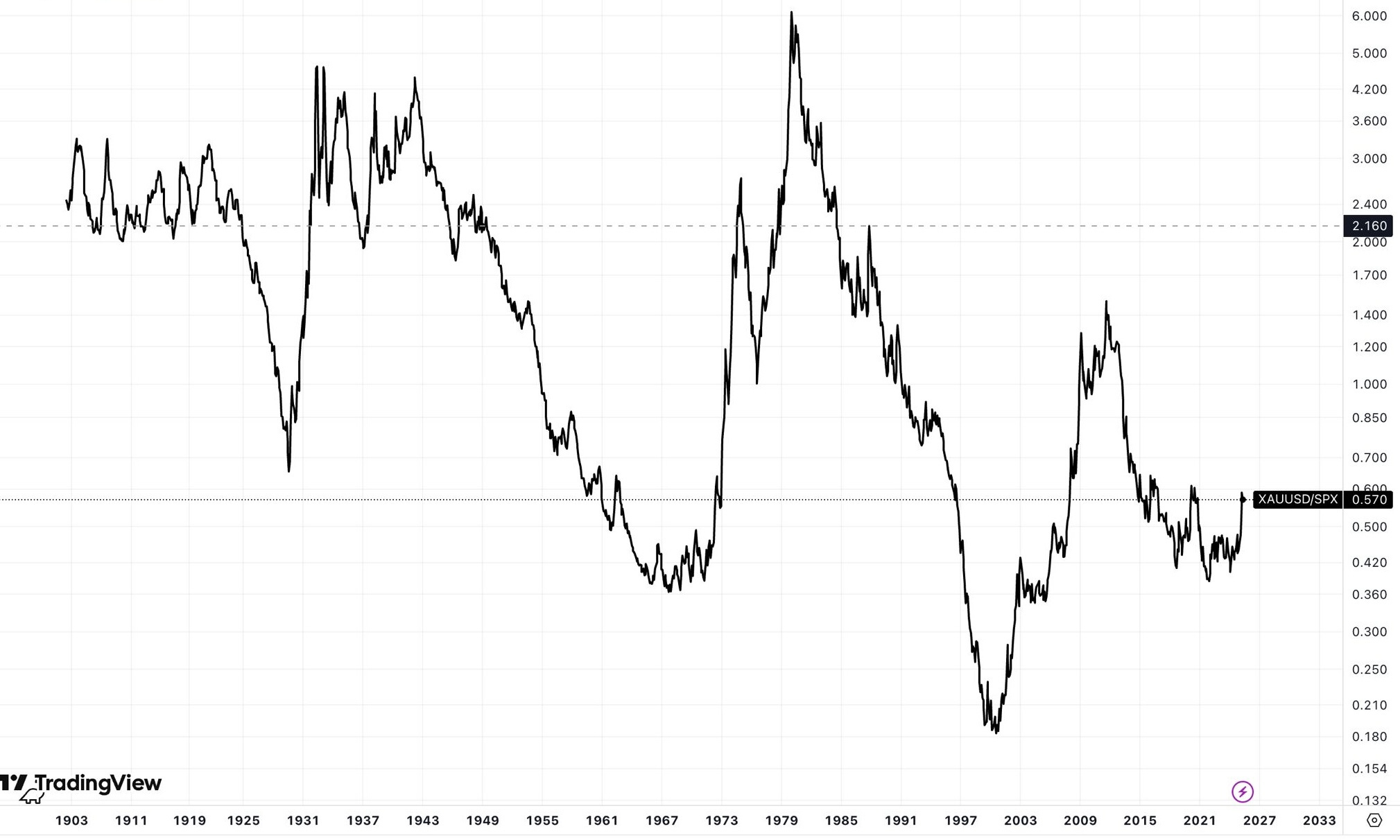

Viewing the chart below comparing the gold price relative to the value of the the S&P 500 U.S. stock index, one can immediately observe a rare pattern predictive of transformational changes being afoot.

In 1929, 1967 and 2000, the ratio of gold to the S&P 500 bottomed prior to earth-shattering events of the time:

1929: the US Great Depression and the tariff-raising Smoot Hawley Act of 1930 unleashing a destructive international trade war;

1967: the loosening of the gold standard until its abolition by US President Richard Nixon in 1971, the introduction of fiat currencies and elevated inflation during the decade of the 1970s; and

2000: China’s admission into the World Trade Organisation and the Dotcom bust in 2001 and the collapse of the subprime mortgage shambles, both in the United States, leading to the 2007-2008 Global Financial Crisis.

Now we see this ratio bottoming in 2021 hinting that something majorly in terms of geopolitics and economics will happen. What could that be is the intriguing question, which I will explore in the next two articles.